I sat in my contractor’s truck once, looking at a quote for a 400-square-foot bedroom addition. The number was $92,000. I remember thinking that seemed absurd for one room. Then he walked me through it line by line foundation, framing, roofing, electrical, plumbing rough-in, HVAC extension and the number stopped feeling absurd. It started feeling like the only honest price for what we were actually asking him to build.

That conversation taught me something most home addition guides skip. The sticker price isn’t the confusing part. The confusing part is figuring out which type of addition actually solves your space problem without overspending on capability you don’t need.

The Three Real Paths to More Space — And Why They’re Not Interchangeable

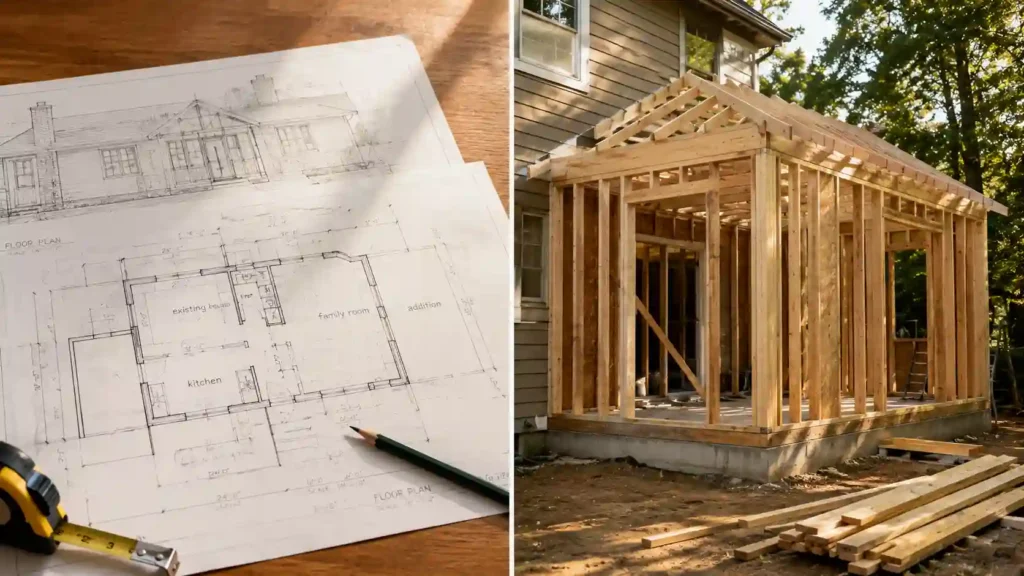

Most people searching for a home addition assume there’s one path: build new space onto the house. There are actually three distinct paths, and they solve different problems.

A home addition extends your current structure with new rooms, a second floor addition, or an expanded wing. The new space connects directly to your existing home, sharing HVAC, plumbing, and electrical systems already in place. This is the only option that genuinely expands the home you already live in if your kitchen is too small or you need a fourth bedroom, an addition is the path that solves it.

Garage conversion takes a different route entirely. Instead of building new, you’re repurposing space you already own but aren’t using for living. A garage conversion ADU transforms an existing garage into a self-contained living unit full bathroom, kitchen, bedroom, the works. Garage conversions are the fastest path at 5 to 9 months from permit to completion, and they’re also the cheapest path into additional living space because the foundation, walls, and roof already exist.

An accessory dwelling unit a detached ADU specifically is the third path. This is new construction on your property, separate from both the main house and the garage. A detached ADU runs $250,000 to $500,000+, considerably more than a garage conversion, but it generates rental income without disrupting your existing garage or home structure at all.

Here’s the distinction that actually matters when deciding: home additions return value only at resale. Garage conversions and detached ADUs generate monthly rental income while you own the property. That single difference changes the entire financial calculation, and most general contractors won’t walk you through it unprompted.

Structural Additions: Bump-Outs, Second Stories, and Dormers

Within the home addition category itself, the structural type you choose drives cost more than almost anything else.

A bump-out addition is the smallest commitment. It extends an existing room outward, typically 2 to 8 feet, without requiring a full foundation. Cantilevered bump-out addition construction extending the structure on a cantilevered structure with no footings — can cut costs even further. Bump-out addition pricing runs $85 to $200 per square foot, and a small bump-out can land as low as $5,000 to $30,000 total. This makes sense for a kitchen island, a dining nook, or a few extra feet in a cramped bathroom.

A second-story addition sits at the opposite end of the complexity scale. Adding a full second story to a single-story home can double your living space, but it comes with serious structural demands. Foundation reinforcement alone can run $5,000 to $25,000 if the existing foundation needs strengthening to support the added weight. Roof replacement during a second-story addition often runs $15,000 to $35,000 since the entire roof structure typically needs to come off. HVAC and electrical upgrades for a second floor addition add another $20,000 to $40,000. All told, second-story addition pricing runs $90,000 to $250,000 depending on square footage and finish level.

One real upside to building up rather than out: second-story building up reduces foundation cost since you’re not pouring new footings across additional ground. Build out reduces cost up to 50 percent vs build up in some cases, but only when your lot has room to expand horizontally. If it doesn’t, building up becomes the only real option regardless of the foundation premium.

Dormer addition construction sits in a smaller, often-overlooked category. Adding a dormer increases attic space and pulls natural light into upper rooms attic dormer natural light addition projects are popular specifically because they convert dead attic space into something usable without the full cost of a second-story build.

Specialty Room Additions and What Drives Their Price Up or Down

Not all home addition projects are equal in complexity, and the room type you’re adding matters as much as the square footage.

Sunroom addition projects sit on the affordable end. A three-season sunroom enclosed with glass but lacking insulation and HVAC runs $10,000 to $40,000. A four-season sunroom, which adds insulation, electricity, and a full HVAC system, costs more but extends usability through winter. Prefab sunroom options start even lower, sometimes under $15,000 for a basic kit. Florida room addition and Arizona room addition are regional variations on the same concept, adapted for climate-specific needs like bug screening or heat management.

Bathroom addition and kitchen addition projects sit at the expensive end of the specialty room category, and the reason is consistent across every source I’ve checked: plumbing. Bathroom addition pricing averages $22,000, with half bathroom addition cost breakdown showing $4,200 to $12,000 for a stripped-down sink-and-toilet version. Kitchen addition costs exceed $50,000 in most cases once cabinetry, appliances, and code-required electrical and plumbing work get added in.

Primary suite addition and master suite addition projects combine a bedroom, a bathroom, and often a walk-in closet into a single high-cost package. Master suite addition pricing runs $175,000 to $254,000 for a basic-to-average build, with upscale master suite finishes pushing past $456,000+ when custom closets and premium fixtures enter the picture. Primary suite first-floor addition projects popular with homeowners planning to age in place carry the same cost profile but add accessibility considerations to the design process.

In-law suite construction runs $44,000 to $100,000 depending on size and complexity, factoring in the kitchen, bathroom, and separate entrance most in-law units require for genuine independence. Mudroom addition and entryway addition projects sit at the low-cost end a 36-square-foot mudroom addition cost runs $3,600 to $7,200, driven mostly by flooring and storage rather than structural work.

ADUs, Garage Conversions, and JADUs: The Income-Generating Alternative

This is where the math gets genuinely interesting, and where most homeowners haven’t done the comparison carefully.

Accessory dwelling unit construction whether a detached ADU, attached ADU, or garage conversion ADU creates independent living facilities on a single residential lot. A junior accessory dwelling unit, or JADU, is a smaller variant, typically under 500 square feet, built within the existing footprint of the primary home. JADU vs ADU comparison usually comes down to size limits and whether you’re adding new square footage or just reconfiguring existing space.

Garage conversion ADU pricing runs $50,000 to $173,000 depending on region and finish level, averaging around $115,000 in most markets. Garage conversion property value increase runs 20 to 35 percent, and garage conversion ROI hits roughly 80 percent among the best returns of any addition type discussed here. The reason is straightforward: you’re not paying for new foundation, walls, or roof. You’re paying to finish and convert what already exists.

Detached ADU construction costs considerably more $250,000 to $500,000+ because it’s genuine new construction requiring its own foundation, framing, utility connections, and permitting process. Detached ADU rental income runs $2,500 to $4,000 per month in many markets, compared to garage conversion’s $1,200 to $3,000 per month. The higher income partially offsets the higher build cost, but break-even detached ADU timing runs around 10 years versus break-even garage conversion at just 4 to 6 years.

ADU above garage construction adding a second story over an existing garage rather than converting the garage itself roughly doubles the cost of a standard conversion, often landing near $350,000. The premium comes from structural realities: most garages weren’t built to support a second story, so additional footings, a licensed structural engineer’s review, and reinforced floor support all get added to the project scope.

California has driven much of the recent momentum here. ADU law has streamlined permitting significantly, and California one in six new homes is ADU now a remarkable shift in just a few years, 90,000+ ADUs permitted since 2017 reflects both the legislative push and genuine homeowner demand. 66 percent of California homeowners considering ADU construction signals this isn’t a fringe trend anymore. ADU zoning, ADU setback requirements, and owner occupancy requirement rules still apply, but they’ve loosened considerably compared to a decade ago. Title 24 compliance remains mandatory in California specifically covering insulation, efficient appliances, and energy documentation that adds to project scope regardless of how the unit gets financed.

Financing a Home Addition Without Guessing at the Math

Almost nobody pays cash for a six-figure home addition project, and the financing options available shape what’s actually feasible.

A home equity loan lets you borrow a lump sum against your home’s existing equity straightforward, predictable monthly payments, fixed interest rate in most cases. A home equity line of credit, or HELOC, works differently a revolving credit line that lets you borrow against equity as needed rather than all at once, useful for projects with phased costs.

Cash-out refinance consolidates your existing mortgage and addition funding into a single new loan, often at a lower rate than a separate construction loan would carry. The tradeoff: borrowing power is limited to roughly 80 percent of current property value, and recent buyers without much built-up equity may not qualify for enough to fully fund the project.

Construction loan and renovation loan products exist specifically for projects like this, disbursing funds in stages as work completes rather than all upfront. FHA 203(k) loan options combine a home purchase or refinance with renovation funding in a single mortgage product, useful for buyers taking on a fixer-upper with addition plans already in mind.

For ADU and garage conversion projects specifically, a three-phase loan structure has become popular: a small cash-out refinance covers design and permitting costs first, a construction/renovation loan covers the build itself, and a final refinance based on the property’s new appraised value including the ADU wraps everything into one long-term mortgage. Home Equity Investment, or HEI, products offer a no-monthly-payment alternative, trading a share of future appreciation for upfront cash, though they typically cost more over a long holding period than a traditional loan.

DSCR loan financing works differently from all of the above it’s not construction financing at all, but a refinancing tool used after an ADU or garage conversion is built and rented. DSCR loan minimum amounts typically run $75,000 to $150,000, and lenders evaluate the property’s rental income against its debt obligations rather than the owner’s personal income. CalHFA predevelopment grant funding, available up to $40,000 in California specifically, helps cover design and permitting costs before construction financing kicks in.

Whatever financing path you choose, build in a contingency fund of 10 to 20 percent above your initial budget. Every contractor I’ve talked to says the same thing: foundation surprises, permit delays, and material cost shifts are the norm, not the exception, on a project this size.

Permits, Process, and the Timeline Nobody Wants to Hear

Building permits and local building codes apply to virtually every home addition project, and skipping this step even on a small bump-out creates real legal and resale risk down the line.

The typical process starts with zoning review to confirm your planned addition fits lot size and setback rules. Structural engineering and a foundation assessment often follow, particularly for second-story additions where foundation reinforcement may be required. Architect fees for blueprint design typically run $2,000 to $10,000, covering the plans your contractor and the permitting office will both need.

Once plans are approved, you’ll move through a combination permit or separate mechanical electrical plumbing permit applications depending on your municipality. A pre-construction meeting with a plan checker or building inspector is standard for ADU and garage conversion projects specifically. Multiple contractor bids at least three give you a real basis for comparison rather than trusting a single number in isolation.

Construction timeline varies dramatically by addition type. Garage conversion timeline runs 5 to 9 months from permit to completion. Second-story addition timeline and detached ADU timeline both run 6 to 12 months, accounting for the additional structural and utility work involved. Post-construction cleanup cost often overlooked in initial budgets typically adds a few hundred dollars to wrap up debris removal once the build itself is done.

Conclusion

Home additions cover far more ground than a single “extra room” concept suggests bump-outs, second stories, sunrooms, primary suites, garage conversions, and full ADUs all solve different space problems at dramatically different price points. The national average lands between $86 and $208 per square foot, but the real decision isn’t about averages. It’s about matching the addition type to what you actually need: a home addition if you want more space in the house you live in, a garage conversion if you want the best ROI and fastest timeline, or a detached ADU if you want meaningful rental income and don’t mind the longer build and break-even period. Get the foundation, permits, and financing lined up before swinging a hammer, and budget that 10 to 20 percent contingency without exception.